A prolonged decline in demand will always bring storage constraints for fuels that need to be stored and shipped before being consumed. Oil has been hit much more quickly than other fuels by the unprecedented demand destruction caused by Covid-19, with prices plunging to historical lows and storage filling up. Liquefied natural gas (LNG) is next in line, a Rystad Energy analysis finds.

Global LNG supply is forecast to reach 380 million tonnes (Mt) in 2020, 17 Mt higher than in 2019. Demand, on the other hand, is expected to rise only 6 Mt from 2019 to 359 Mt according to Rystad Energy’s current estimate, as industrial activity has declined due to the pandemic.

The consumption, or demand, is more flexible for LNG than for other fuels as different fundamentals such as weather can rapidly change during the year. If the world faces a colder-than-forecast winter and lockdowns are lifted faster than expected, then demand will see a boost. The opposite could happen if the winter is milder or if resumption of industrial activity sees further delays.

Normally a reasonably oversupplied market is not necessarily a problem as buyers take advantage of the lower prices to utilize more gas for power generation and to store gas/LNG after the winter season. But in 2020, when ample LNG supply is coupled with demand destruction, prices have already hit record lows and storages have already filled faster than usual. Production shut-ins are becoming a realistic possibility.

Europe became the de facto global LNG sink in 2019, when the milder-than-expected winter slowed down LNG demand growth in Northeast Asia. Europe imported about 80 Mt of LNG in 2019, an 80% increase from 2018. In the first two months of 2020, when the coronavirus pandemic hit Northeast Asia heavily, Europe managed to increase LNG imports by 35% compared to the same period in 2019, mainly driven by the UK, Spain and Belgium.

The impact on LNG imports to other European countries has not been as significant as initially expected, however. European demand has been rather resilient to Covid-19 as buyers stock up on cheap supplies: The continent realized a monthly record-high LNG import of 8.9 Mt in March, a 20% year-on-year increase.

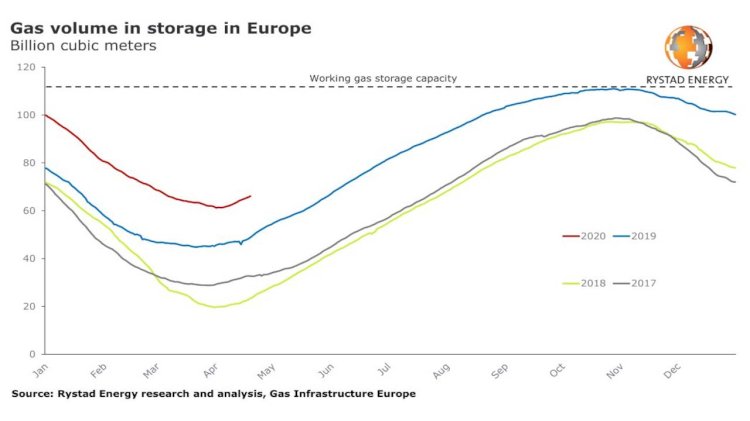

Where is the problem? Gas storage space is a key factor for Europe’s ability to absorb excess LNG volumes. At the end of March 2020, about 62 billion cubic meters (Bcm) of gas was in European storage, 16 Bcm higher than in March 2019. If gas storage approaches top capacity at the end of the filling season, as was the case at the end of October 2019 (98% full), European gas inventories now only have space for some 48 Bcm of gas before winter 2020.

Front-month gas contracts at the TTF trading point in the Netherlands have been trading below $2 per million British thermal units (MMBtu) in April, suggesting that gas traders could take advantage of the historical low gas prices and fill Europe’s storage facilities faster than usual. As a result, European storage could reach its limit and LNG cargoes with deliveries in the summer months are at risk of being canceled.

And the continent’s demand is not growing much either. Europe consumed 554 Bcm of natural gas in 2019, 13 Bcm more than in 2018, primarily driven by coal-to-gas switching in the power sector. Rystad Energy expects European gas consumption to remain at the 2019 level, with a possible mild increase in the power sector. Not much, though, as the coal-to-gas switching in is well maxed out.

Xi Nan, Vice President for Gas and Power Markets at Rystad Energy, says:

“Asia is not likely to take up the full slack. Europe will be under serious pressure to absorb LNG, but it looks like this will be tough given storage levels, lower demand, and the cost of sending it there, especially from the US. If global gas prices slip even further in 2020, this could translate into potential LNG shut-ins.“

In Asia, the signed term contracts can provide Japan and South Korea with enough LNG, meaning the two countries don’t need much gas from the spot market. Chinese LNG buyers, including smaller players, are able to absorb some excess volumes, but less than the expected levels before the pandemic. India is expected to continue utilizing low gas prices and purchase spot cargoes only when the lockdown is fully lifted.

Rystad Energy still doesn’t have an end date for when Europe will completely re-emerge from lockdown, and the impact will probably be deeper coming into the summer months. With gas storage tanks already almost filled to the brim, Europe’s capacity to import and actually use the same amount of LNG as in 2019 seems like a tall order, especially if we see another mild winter.

{kind=link}