Reefer container equipment availability will remain tight over the next few years which will impact shipping capacity supply and freight rates at seasonal peaks, according to Drewry’s latest Reefer Shipping Annual Review and Forecast 2019/20 report, published this month.

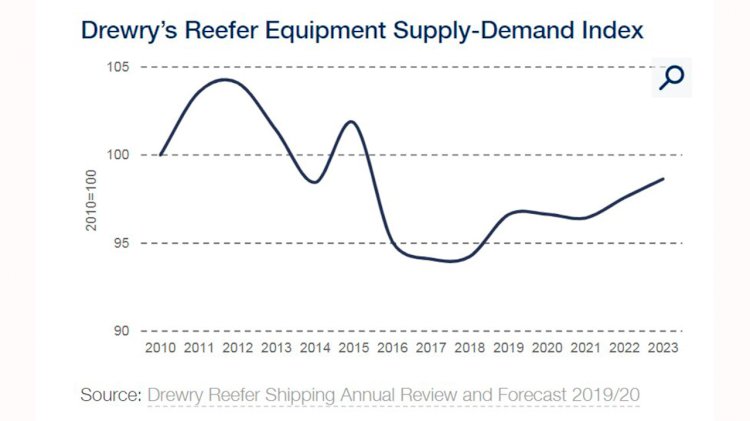

After the dramatic halt in reefer equipment expenditure by cash-strapped shipping lines in 2016 which led to acute shortages in several regions, production of new refrigerated container equipment recovered during 2017 and continued to gather pace in 2018. Drewry expects the reefer container equipment fleet to maintain a CAGR of 4.5% over the next five years which is slightly ahead of anticipated growth in containerised cargo traffic but will not be sufficient to bring supply back into equilibrium – see chart below where 100 equates to equilibrium.

By contrast, there remains ample supply of containership reefer slot capacity on most trades, though certain routes with a high proportion of reefer cargo can experience tight space during seasonal peaks.

Drewry’s director of research products Martin Dixon said:

“While we expect container carriers to continue to improve the effective availability of reefer containers through more centralised inventory and imbalance management, Drewry’s data indicates that equipment supply conditions will remain tight. With cargo owners increasingly reliant on container carriers to move perishable products, given the ongoing decline in the specialised breakbulk reefer shipping fleet, refrigerated shipping capacity could be constrained during seasonal peaks.”

Global seaborne reefer trade continued to grow in 2018 but the pace of expansion was slower than trend and is projected to be more muted over the coming years. Drewry estimates that the volume of seaborne reefer cargo grew 3% in 2018 to 129 million tonnes which was weaker than the 4.4% gain achieved in 2017 and the 3.5% average annual rate recorded over the prior 10-year period. The weaker trade development was driven by a slowdown in shipments of meat and poultry, fish and seafood, and banana shipments, as well as a contraction in deciduous trade.

Looking ahead, Drewry forecasts that worldwide seaborne perishable reefer trade will continue to expand but at a below trend rate of 2.7% a year in the period to 2023 as certain seasonal climate related factors such as El Nino slow production output in the short term and rising geopolitical risk impacts wider trade growth prospects. But containerised reefer traffic will expand at a faster pace as its share of the trade is forecast to rise from 81% in 2018 to 85% by 2023 as the specialised breakbulk reefer shipping fleet continues its contraction.

Martin Dixon said:

“Hence, despite a slowdown in the pace of growth in global seaborne perishable cargo trade, the additional boost of modal shift is providing container carriers with an attractively expanding market in reefer cargo. Excluding a particularly weak 2019 caused by certain one-off weather related factors, forecast growth thereafter is expected to match that of the wider container shipping market with annual growth of around 4%. And together with tight container equipment availability we expect reefer container freight rates to continue to outperform dry box rates.”

{kind=link}